Most freelancers learn finance in the worst possible way. By getting it wrong once.

The first time a tax bill lands and you do not have the money set aside. The first time a client goes silent for sixty days and rent is due in seven. The first time you realise you have been running profitable months and broke quarters at the same time, and you cannot explain the gap to yourself.

These are not unusual stories. They are the standard onboarding for anyone who leaves a salary and starts billing their own clients. Schools do not teach this. Most personal finance content does not cover it because freelance finance is not personal finance. Most corporate finance content does not cover it because freelance finance is not corporate finance either. There is a middle layer that almost nobody writes about clearly, and that middle layer is where the entire one-person business economy lives.

This guide is for that middle. The freelancer with three to fifteen clients. The independent consultant. The solo designer, developer, writer, coach, translator, photographer, agency-of-one, anyone billing in their own name. You do not need to become an accountant to run the financial side of a business like this. You do need a system. The rest of this piece is the system.

Freelance finance is its own category, and that is the first thing to understand

Personal finance assumes a salary. A predictable monthly amount lands in your account, you budget against it, you save what is left. The whole model is built around stability of income and unpredictability of spending.

Corporate finance assumes the opposite. Cash comes in lumpy from many sources, goes out in highly predictable patterns, and a finance team manages the gap with forecasts, reporting, and access to credit.

Freelance finance has neither shape. Income is lumpy and unpredictable. Spending is mixed, half personal and half business, half predictable and half emergency. There is no finance team, no credit line, no salary buffer, and the same person is selling the work, doing the work, invoicing the work, chasing the payment, paying the tax, and trying to plan next month. The only person who could spot a problem early is also the person too busy to look for it.

Most software in this space pretends freelancers are tiny companies. They are not. A company has structure, division of labour, and time. A freelancer has none of the three. Any system that ignores that asymmetry will be abandoned within a month. The system you actually need is the smallest possible structure that keeps you in control of five things.

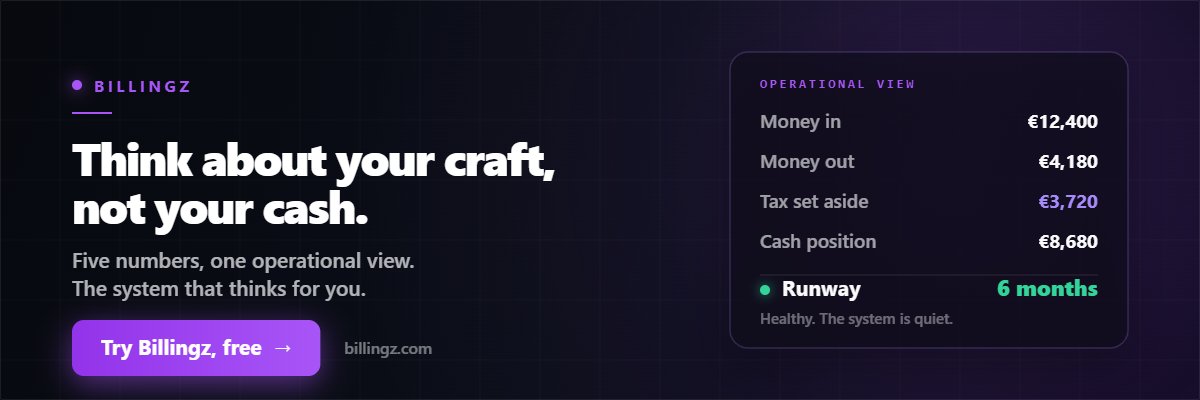

The five things you actually need to track

Forget anything anyone has told you about charts of accounts, double-entry bookkeeping, or quarterly variance analysis. As a freelancer, there are five numbers that matter. Track these and you will know more about your business than most operators around you.

Money in. What clients paid you, when they paid, and whether any of it is still outstanding. This is your income and your accounts receivable in one view.

Money out. What you spent on business operations, separated from personal spending. Software, subcontractors, travel, equipment, anything you would not have bought if the business did not exist.

Tax exposure. What you owe the tax authority right now if everything stopped, including income tax, VAT or equivalent sales tax, and any social charges. Not what you will owe at year-end. What you owe today.

Cash position. What is actually in your bank account, minus the tax exposure above. This is your real working capital, the money you can spend without consequence.

Runway. How many months you can keep operating at current spending if no new income arrived starting tomorrow. This is the only number that matters when something goes wrong.

Most freelance software gives you the first two and ignores the other three. Most freelancers focus on the first one and forget the other four. The whole point of a financial system is to keep all five visible without you having to think about them between client deliveries.

Invoicing, and the cost of one missed week

Invoicing is the part everyone gets close to right. Most freelancers send invoices, most freelancers eventually get paid, most freelancers think this is the hard part of finance. It is not. It is the easiest part. The hard part is the timing, and the timing is what nobody teaches.

A client who pays 30 days after you invoice is not paying you 30 days late. They are paying you on time according to a standard contract you probably agreed to without reading. The clock only starts when you actually send the invoice. If you invoice three weeks after the work was done, you are now sitting at 51 days from work delivered to money received. If the client then takes an extra week, you are at 58 days. Over the course of a year, that delay compounds into thousands of euros of working capital sitting on someone else's balance sheet.

The fix is mechanical, not strategic.

Send invoices the same week the work is delivered, ideally the same day. Not at month-end. Not when you remember. Use net-14 terms by default. Net-30 is a holdover from corporate accounts payable. You are not a corporate vendor with a credit line. You are a person who needs the money. Send a polite reminder the day before the invoice is due. Send a firmer one the day after. This is not aggressive. This is normal business. Charge late fees, and mean it. Even a small fee changes a client's mental model of your invoices from "I will get to it" to "this one has a clock on it."

A freelancer who tightens invoicing terms from net-30-loose to net-14-tight typically improves cash position by 20 to 40 percent within a quarter, without earning a single extra euro.

That is not a finance trick. That is just refusing to lend money to your clients for free.

Taxes when you are not on payroll

When you had a salary, taxes happened to you. Money came out before you saw it, the rest landed in your account, and you mostly did not think about it. The brain learns over a few years to treat the post-tax number as "your money."

When you are self-employed, that wiring is gone. Every euro that lands in your account looks like yours, because it is. But a meaningful slice of it belongs to the tax authority, and you are now the one responsible for separating the two. Almost every freelance disaster starts with someone forgetting this.

The working rule is to set aside between 25 and 40 percent of every payment into a separate account the same day it arrives. The exact percentage depends on your country, your tax bracket, your VAT status, and your business expenses, and an accountant should calibrate it for you once. After that, the rule is automatic. Money in, percentage out, into the tax account. Do not touch the tax account except to pay tax. Treat it like it never existed.

This sounds primitive. It is. Sophisticated systems exist, but they all fail when a freelancer is busy. The percentage rule works because it requires zero thinking under pressure. Done daily, it removes 90 percent of tax stress from the calendar.

A few specific traps that catch most freelancers. VAT (or sales tax) does not belong to you. If your country requires you to collect VAT on invoices, that money is being collected on behalf of the state. It is not income. Treat it the same as the income tax set-aside, ideally in its own sub-account. Quarterly payments compound. If you owe taxes quarterly and miss one, the next one is rarely "double next quarter." It is usually that quarter plus penalties plus interest. The system does not forgive. Year-end is the wrong horizon. A freelancer thinking "I will figure out taxes at year-end" is committing to a worst possible scenario: ten months of cash that feels like income, then a brutal bill in March. Monthly tax accounting prevents this entirely.

You do not need to understand the tax code. You need to make sure the money the tax authority will eventually claim is never in the same place as the money you can spend.

Cash flow versus profit, and why profitable freelancers go broke

This is the single most misunderstood concept in freelance finance, and it kills more independent operators than any other single mistake.

Profit is what you earned over a period. Cash flow is what actually moved through your bank account over that period. They are not the same number, and the gap between them is where careers end.

Imagine a freelancer who, in a single month, delivers €15,000 of work. On paper that is a strong month. Profitable. Worth celebrating. But the clients pay on net-45 terms, the bills for the freelancer's own subcontractors are due on net-14, the rent comes out on the first, the VAT payment is due on the fifteenth, and the freelancer also took a holiday booked three months ago. The €15,000 will arrive eventually. The €11,000 in outflows is happening now. That freelancer is profitable on paper and insolvent in real life, for somewhere between six and ten weeks.

This is not an edge case. It is the default condition of freelance life. Profitable months and broke quarters are the rule, not the exception. The reason most freelancers cannot explain it to themselves is that they are tracking the wrong number. They are looking at what they billed. They should be looking at what cleared and what is still owed.

A working freelance system separates these two views. The earned view shows what you delivered and invoiced, regardless of when it pays. The cash view shows what actually arrived in your account and what is leaving. You need both. The earned view tells you whether the business is healthy. The cash view tells you whether you survive the next sixty days. Most freelancers see only one or the other. Both are necessary, and the gap between them is where you actually live.

Runway, but for one-person businesses

Startups talk about runway constantly. Freelancers almost never do, and this is one of the reasons freelance life feels so much more stressful than it needs to feel.

Your runway is the answer to a simple question. If no new client signed today, and your existing clients all paused, how many months could you keep operating at current spending? Calculate it once, and you will see the freelance life differently within an afternoon.

The calculation is straightforward. Take your cash position (real cash in the bank, minus tax exposure). Divide by your average monthly outflow (business plus personal, since you are the same legal entity). The result is your runway in months.

Two months of runway is the danger zone. You are one slow client away from real problems. Four to six months is a comfortable working position. Eight months or more is excellent and probably means you have either been lucky, conservative, or both.

The single most useful habit a freelancer can build is checking runway weekly. Not monthly. Not quarterly. Weekly, in five seconds. Because runway does not collapse slowly. It collapses in a week, when a client cancels and another delays and a tax bill lands and suddenly you have gone from six months to two.

Knowing your runway does not make the runway longer. It makes you behave differently while it is healthy.

You take better clients. You raise rates earlier. You say no to bad-fit work. You stop accepting net-60 because you can afford to. The number does not change your money. It changes your posture.

When to bring in help, and what kind

There are three kinds of help available to a freelancer, and most operators pick the wrong one at the wrong time.

An accountant. Useful for setup, tax filing, and corner cases. Bad investment for ongoing financial visibility, because they look at last quarter, not this week. Hire an accountant once, get the structure right, then see them quarterly. Do not pay an accountant to do the work a tool should do.

A bookkeeper. A bookkeeper categorises transactions and keeps your books current. Worth it once your monthly transaction count goes over about 50, or once you stop keeping up. Cheaper than an accountant, more frequent, more useful for cash visibility.

A tool. This is where most of the day-to-day work belongs for a freelancer in 2026. A good operational tool gives you the five numbers above, in one place, updated automatically, without you needing to learn accounting. Not a spreadsheet you maintain. Not five separate apps that each do one thing. An environment that shows you where you stand right now, what needs attention, and how much runway you have.

The honest order, for most freelancers: tool first, accountant second (once a year), bookkeeper third (only if volume justifies). Reversing this order is the most common and most expensive mistake.

Building a system that thinks for you

The whole point of a freelance financial system is to remove your need to think about it between client deliveries. Most days, the system should run quietly. You glance at it. You see where you stand. You move on with your day.

This is what we have been building Billingz around. Not a feature list. Not an accounting product in disguise. A working environment where a freelancer can see all five numbers at once, where the tool tells you what needs attention before it becomes a crisis, where invoices, payments, taxes, and runway are not five separate apps but one operational view.

When cash is healthy, the system is quiet. When something needs your attention, the system tells you what and why. This is what operational clarity looks like in practice. Not more dashboards. Not more notifications. The smallest possible structure that keeps you in control of the five things that actually matter.

The product is not the point of this essay. The point is that whatever system you build or buy, it should do this kind of work for you. The freelancer who has to think about finance in order to know how the business is doing is using the wrong system.

You do not need to become an accountant to run the financial side of a freelance business. You need a working method, a small number of habits, and a tool that does the unsentimental tracking quietly in the background. The five numbers stay visible. The tax money stays separated. Invoices go out the same week the work is done. The runway gets a glance every week.

That is the whole job. Everything else is detail.

The freelancers I know who run calm, profitable, sustainable businesses are not financially sophisticated people. They are just people who have built the smallest possible system that prevents the next disaster, and then they get on with the work. That is the goal here. Not financial expertise. Operational calm.

Build that, and you will spend the next decade of your career thinking about your craft instead of your cash.

Frequently asked questions

This essay is general information based on operating experience, not personalized financial, tax, or legal advice. Consult a qualified accountant or tax advisor for guidance specific to your situation.

A freelance financial system that does this work for you, quietly.